Breaking Down the Income Tax Bill 2025 : Key Changes and Implications for Taxpayers

The Indian Government has introduced the Income Tax Bill 2025, a landmark reform designed to replace the Income Tax Act of 1961. This initiative aims to modernize the tax framework, simplify compliance, and accommodate the dynamic needs of businesses and taxpayers. Here's a detailed summary of the major provisions and changes, including the definition of the tax year and audit requirements.

Key Updates in the Income Tax Bill 2025

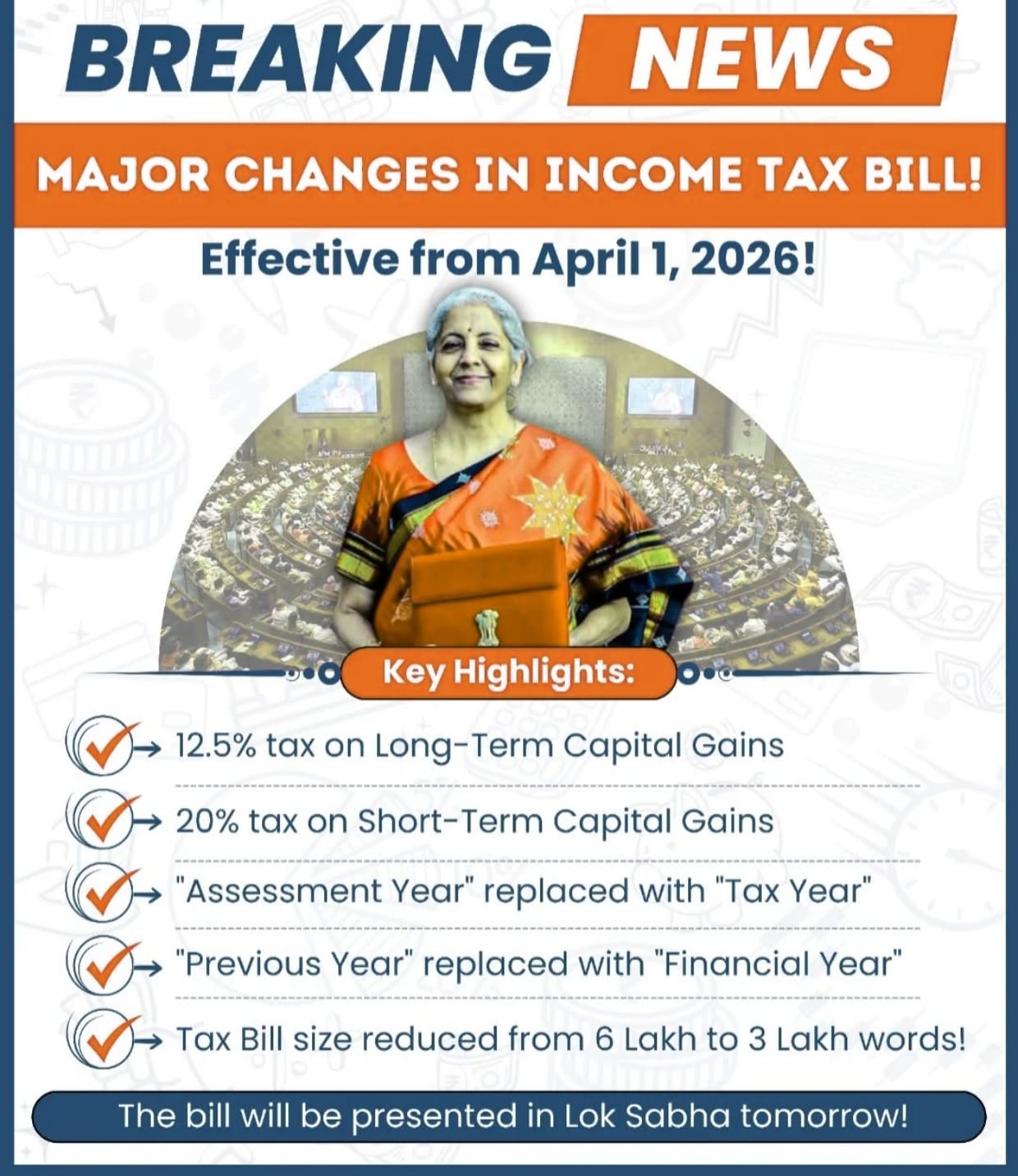

1. Tax Year

The definition of the "tax year" has been clarified and expanded in the new Bill:

- Standard Tax Year: The tax year refers to the 12-month period starting from April 1st and ending on March 31st.

- For New Businesses or Income Sources: If a business or profession is newly established, or a new source of income arises during the year, the tax year:

- Begins on the date of establishment or income realization.

- Ends with the conclusion of the same financial year.

- Alternate Tax Periods: In special cases, a 12-month tax period ending on a date other than March 31st may be allowed for companies following foreign tax laws.

This streamlined definition ensures clarity for taxpayers while accommodating new businesses and income sources.

2. Tax Audit Provisions (Clause 63)

Tax audits continue to play a critical role in ensuring compliance with income tax regulations. Here’s a summary of the requirements:

Who Needs a Tax Audit?

- Businesses with total turnover exceeding ₹10 crore, provided at least 95% of transactions are conducted digitally.

- Businesses with turnover above ₹1 crore, where digital transactions are below 95%.

- Professionals with gross receipts exceeding ₹50 lakh annually.

- Entities opting for presumptive taxation but declaring profits lower than prescribed.

- Eligible businesses claiming deductions under specific sections (e.g., tea, coffee, or rubber development accounts).

- Non-profit organizations and specified assessees whose income exceeds the maximum amount not chargeable to tax.

What Does a Tax Audit Involve?

- Examination of books of accounts by a qualified accountant.

- Submission of an audit report one month before the income tax return filing deadline.

- Verification of compliance with tax provisions and proper maintenance of financial records.

Purpose of Tax Audits:

- Ensure accuracy in financial reporting.

- Detect instances of tax evasion or avoidance.

- Enhance transparency and adherence to legal provisions.

Non-Compliance Penalties:

- Up to ₹1,50,000 or 0.5% of turnover, whichever is lower, for failure to conduct audits.

- Additional penalties for failure to maintain proper books or furnish reports.

3. Broader Changes and Additions

Capital Gains and Deductions

- Detailed rules for capital gains, including company share buybacks, agricultural land transfers, and compulsory acquisitions.

- Special deductions for industries engaged in infrastructure development, housing projects, and renewable energy initiatives.

Heads of Income

The Bill categorizes income under the following heads:

- Salaries

- Income from House Property

- Profits and Gains from Business or Profession

- Capital Gains

- Income from Other Sources

International Transactions and Non-Residents

- Introduction of advance pricing agreements for better clarity on international tax matters.

- Taxation of royalty, fees for technical services, and presumptive taxation for certain non-resident businesses.

Digital Economy Provisions

- Taxation on foreign digital businesses under the Significant Economic Presence (SEP) principle.

- Enhanced monitoring of crypto asset transactions with mandatory reporting.

Mode of Payment

The Bill emphasizes digital transactions and discourages cash dealings, providing clear rules for:

- Loans, deposits, and payments above specified thresholds.

- Electronic modes for tax payments and deductions.

Why the Income Tax Bill 2025 Matters?

The new Bill is a comprehensive overhaul of India's tax structure, aimed at:

- Simplifying compliance for individuals and businesses.

- Promoting the digital economy by incentivizing electronic transactions.

- Strengthening transparency and tackling tax evasion.

- Facilitating global business transactions with streamlined international tax provisions.

For more insights, visit the following trusted sources

Conclusion

The Income Tax Bill 2025 is a transformative step toward a modern and inclusive tax regime. By staying informed about these updates, individuals and businesses can ensure compliance and optimize their tax planning.

Disclaimer

This blog reflects my understanding of the draft Income Tax Bill 2025. The official New Income Tax Bill is scheduled to be presented in Parliament tomorrow, February 13, 2025. Any document circulating on WhatsApp and social media before this date may be unofficial and may not reflect the final provisions of the bill.